Payments Intelligence: A Pioneering Approach to Leveraging Payments Data

Abstract

The payments industry continues to change and evolve. Developments in new rails (e.g., real time), new standards (e.g., ISO 20022), and new business models (e.g., connected commerce, embedded finance) mean payments are starting to carry rich transaction data and are becoming more granular, cheaper, and faster, and less of a friction point in the customer’s journey. As a result, payments can give organizations an unparalleled insight into their customer behavior in real time, presenting a business opportunity.

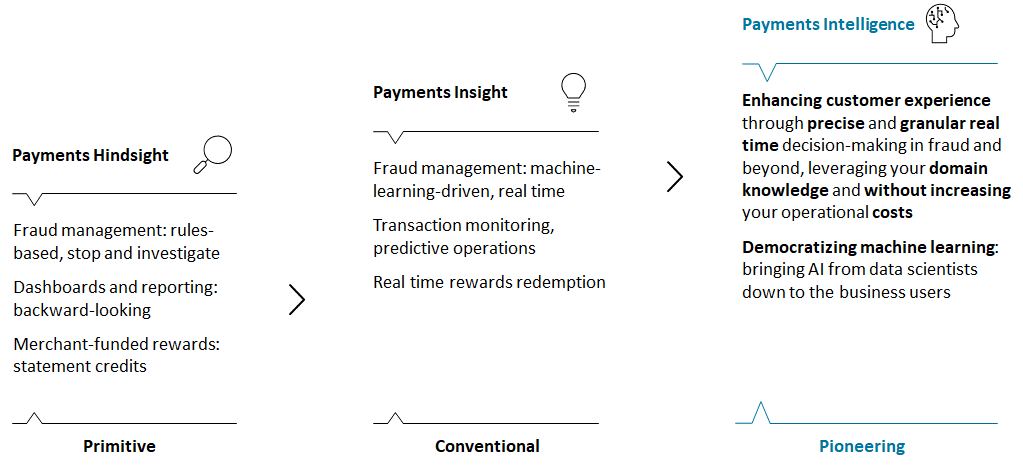

The idea of making use of payments data is not new. However, the industry is still in transition from payments hindsight (backward-looking, not real time) to payments insight (real time for fraud management and limited other insights). Now, the leaders can go to the next level—payments intelligence—and find the way to enhance customer experience through precise and granular real time decision-making in fraud and beyond. Payments intelligence is much more than payments data monetization; it turns every payment into a business opportunity.

Real time decision-making is difficult, especially when multiple parties are involved: precision is essential, while inaction is costly. Many have turned to artificial intelligence (AI) and machine learning (ML) models, especially in fraud management. However, many challenges remain with conventional approaches, such as obtaining and sharing data, or acquiring deep specialist expertise needed to develop and train ML models, resulting in high costs and suboptimal decision-making.

An alternative pioneering approach—payments intelligence framework, where multiple participating entities share their learnings via signals delivered as a “payments DNA” string—can help address those challenges and deliver significant benefits: The cost and effort can be reduced by more than 80% while delivering an enhanced customer experience. The framework enables the entire ecosystem to speak the common AI language and leverage the domain expertise of others’ without having to share or acquire data.

Banks, merchants, and payment providers should determine where they would benefit the most from improved precision in real time decision-making, consider the relevant domain and data science expertise they have and how they can close any gaps, and seek out partners that share the vision outlined in this report.

Related Research

Harnessing the Benefits of AI in Payments: Unlocking a Range of Workflow and Product Enhancements

Push Payments Fraud: Deal with It or Regulators Will Intervene

Swedbank: Modernizing Card Fraud Management and Improving Customer Experience

Technology Trends Previsory: Retail Banking, 2024 Edition

Next-Gen Card Issuer Processors in the US: Ready to Capture Credit Card Opportunity?

The Siren Song of Credit Card-as-a-Service: In Search of a Breakthrough Opportunity in the US Market

Is This the "End of History" Moment for Bank Card Issuers? Leading in the Disruptive World of Cards

Modernizing the US Card Processing Platforms: Stories of Digital Transformation