Dimensions: North American Retail Banking IT Pressures & Priorities 2024

Investing in Data and New Business Models

Key research questions

- What priorities are driving technology strategy for banks in North America in 2024?

- What are the leading product and technology investment areas?

- How will the compliance burden affect product development?

Abstract

North America has long been one of the largest and fastest moving regions in terms of technology investment, and 2024 will be no different. IT budgets have grown by an average of 5% on average compared to 2023, and expectations are positive for spending to increase by an even greater amount in 2025. While the plans of individual banks can differ quite sharply, there are several themes that will drive activity across the region as a whole.

The first is meeting what is a growing list of regulatory requirements. From customer protection to open banking and payments, banks in both the US and Canada will need to devote significant resources to remaining compliant. Alongside this is a strong emphasis on enhancing products and experiences for customers. Consumer and small business digital channels will be important focus areas, alongside exploring the opportunities in BaaS and embedded finance.

When it comes to the underlying technologies that will support these projects, there will be a continued emphasis on data management, AI (including Gen AI), automation, and cloud technologies. Investments in these areas will support a range of outcomes, but all underscore the broader cultural change that has taken place in the industry as financial institutions seek to become increasingly agile in the face of competitive challenges and new market opportunities. While many have already seen past investments pay dividends, there is often further to go and driving real change is never a ‘once-and-done’ activity.

To shed light on the business pressures and technology priorities of the industry, Celent has completed its third global survey of senior executives at retail banks: The Celent Dimensions Survey 2024. This study captures the insights and opinions of 63 respondents at financial institutions across Canada and the US to provide an in-depth view into attitudes across the region, as well as highlighting the leading technology priorities for the year ahead and the products and processes that will see the greatest change.

Key findings include:

- 60% believe that the competitive threat from fintechs and other challengers is increasing.

- 51% report that meeting compliance and regulatory requirments one of the three most important drivers of their technology strategy, ahead of enhancements to the customer experience (46%).

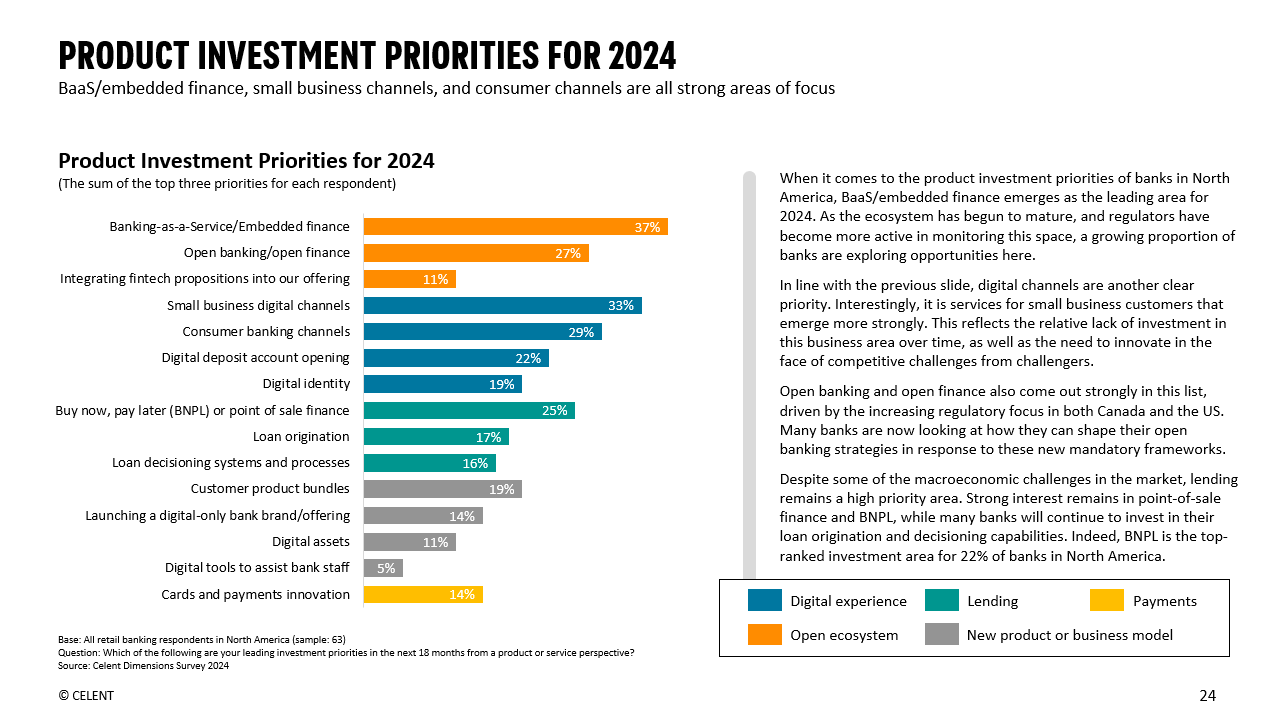

- 37% have highlighted investing in BaaS and embedded finance as a key product-level priority, ahead of investments in consumer and small business digital channels, open banking, and lending.

- 62% are exploring new use cases related to AI technologies.

- 62% state that they expect to launch new customer-facing services using Gen AI in 2024.

The lessons for the industry are clear. Funding innovation is a major strategic driver for banks across all regions in 2024, and those that fail to keep up risk falling behind.

Related Research

Dimensions: Retail Banking IT Pressures & Priorities 2024

May 2024

Dimensions: Retail Banking IT Spending Forecasts by Technology 2024-2029

May 2024

Dimensions Webinar: Retail Banking IT Pressures & Priorities 2024 Edition

May 2024

Dimensions: European Retail Banking IT Pressures & Priorities 2024

June 2024

Dimensions: Corporate Banking IT Pressures & Priorities 2024

May 2024