Independent Producer Survey: Technology, Services, and Other Drivers of Producer Choice (Life/Annuity/LTC/Health Edition)

Abstract

Independent Producer Survey: Technology, Services and Other Drivers of Producer Choice (Life/Annuity/LTC/Health Edition)

The continued growth of the independent agent channel in North America means that competition among carriers for producer mindshare is fierce. The question of carrier choice by producers continues to be important. In most lines, if companies are to grow, they must earn the business from someone else.

In a new report, Independent Producer Survey: Technology, Services, and Other Drivers of Producer Choice (Life/Annuity/LTC/Health Edition), Celent details the answers to important questions about agents’ decision-making. Over 250 independent agents completed a 27-question survey designed to explore their use of technology and the criteria for placement of business with carriers.

This report examines several key questions:

- What do agents want from carriers in services and technology?

- If given an equal (or almost equal) price, what factors matter the most to an agent when they place business?

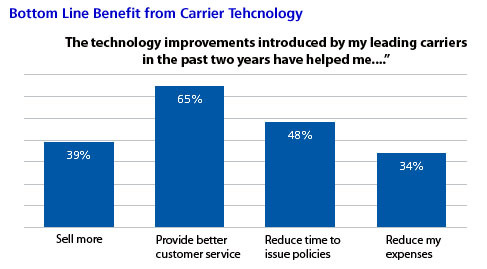

- How are the investments by carriers in agent technologies making a bottom line difference in agencies?

Agents responding to the survey were North American enterprises engaged primarily in life/annuity/LTC/health product distribution. Most individuals fit a common profile: a veteran insurance professional generating a significant book of business from multiple carriers. The producers were asked to identify their "favorite carrier" and give the reason for their choice. These responses are aggregated and insights are offered as to the impact of the data.

The results demonstrate a clear preference by producers for technology that helped them improve service to their customers.

This report is a continuation of the research Celent has done in insurance distribution in general and carrier choice specifically.

"The data is useful for many groups involved in the industry," says Craig Weber, senior vice president with Celent’s insurance practice and co-author of the report. "Differentiation, real or perceived, is critical."

"Carriers can use the report to guide their decisions regarding competing investments in agent technology," adds Mike Fitzgerald, coauthor of the report. "Agents can compare their experience with their peers to benchmark performance. Information technology vendors can test their product blueprints against current and future agent preferences."

The report is 40 pages and contains 28 figures and four tables.

A table of contents is available online.

of Celent's Life/Health Insurance and Property/Casualty Insurance research services can download the report electronically by clicking on the icon to the left. Non-members should contact info@celent.com for more information.